English Farming and Covid-19 Business Update – Autumn 2020

Welcome to this quarter’s Farming Update, which is produced by our Farming Research Group and reports on market and administrative issues that affect farmers’ business decisions and on which they may need to act.

MARKET UPDATE

ARABLE CROPS

Global: Grain Production Report

The FAO – (the Food and Agriculture Organisation of the UN), are predicting, in spite of uncertainties brought by the Coronavirus pandemic, that the global supply and demand of cereal grains will increase this year. Production is set to beat last year’s record by 1.7%. Demand is also set to increase (mainly lead by higher consumption of maize products by livestock), but not in pace with production, leading to growing global stocks to around 895.5 Million tonnes. Notably it is estimated that 47% of this stock is held in China.

The positive predictions for global cereal production are driven by foreseeable record harvests in Canada, and record-high predictions for Brazil and Argentina. Maize production is driving this growth, and this will outweigh lower wheat production following difficult growing conditions in the EU and elsewhere in the Northern Hemisphere such as Ukraine

On a positive note for Global Wheat productivity, Guinness World Records has verified a new world record for wheat yield, south of Christchurch in New Zealand at 17.398 Tonnes per hectare. Jealous British farmers should note that this crop was grown on irrigated land, and the average yield for that area is already an impressive 12 Tonnes per hectare. Something to work towards though!

UK MARKETS

Wheat

UK Wheat harvest saw a 15% yield reduction per ha from the 5-year average according to the UK Centre for Ecology and Hydrology, who also found that this is in combination with a 44% reduction in the winter wheat area from the 5-year average. The quality of wheat seemed to have been good, (which is to be expected from a low yielding crop), that is up until the rain in Autumn when harvest progress was hampered and the wheat arriving later in store seems to have had a lower quality with problems such as sprouting and poor hagberg falling numbers (FWi).

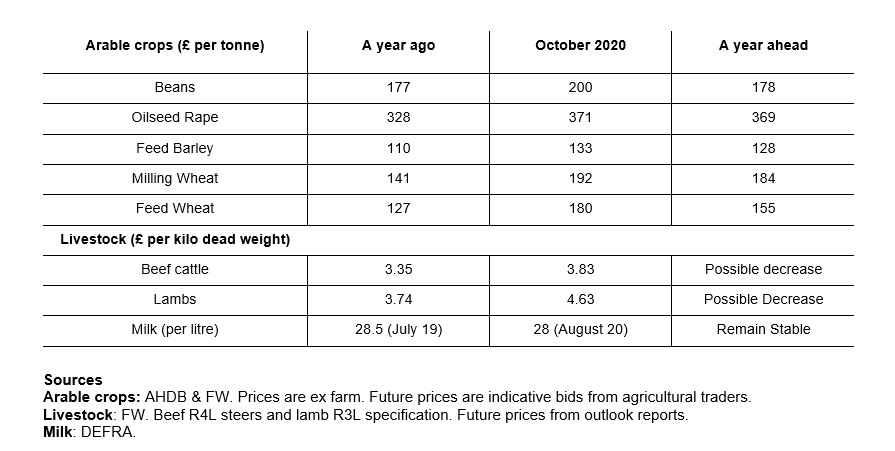

Even before the news arrived that the crop diversification rule under the “greening” element of the basic payment scheme has been dropped by DEFRA the drilled area of Winter Wheat for the next harvest was likely to be large. It is likely to be even greater now, particularly if good weather prevails through the autumn. The news will likely lead to a fall in wheat futures for Autumn 2021 (November 2021 prices are at £153/T, whereas November 2020 prices are at around £180/T). As such farmers would be advised consider selling forward a proportion of their expected crop at these levels.

Barley

Winter barley suffered a similar fate to winter wheats across the UK. With less than 45% of the planted area in good or excellent condition, the AHDB estimated that national yield was well below the 5-year average. Due to poor tillering, the nitrogen contents of winter malting barley have been high (reaching above 2% in the East of England), meaning that very little achieved malting specifcation. AHDB’s yield estimates for winter barley are at 6.5T/ha – 6.7T/ha, compared with 5 year average of 7.1T.

Spring Barley, as a cropping option, mopped up much of the area this spring which had previously been intended for winter crops, The AHDB’s predicted increase of 29% from 2019 on national production is not reflective of outstanding yields, but simply a larger area. The heavy and prolonged rains in August meant many crops suffered from lodging, and most crops still in the field at that point saw germination fall away, rendering a large proportion of the spring crop good only for the feed heap. Like winter barley, spring crops have also seen higher than usual nitrogen levels, to complete the difficult picture for cereal producers this year. AHDB’s yield estimates for Spring Barley are at 5.7T/ha – 6.1T/ha , compared with 5 year average of 5.8T

Much of the surplus of feed barley will need to be exported, and the supply and demand matrix means that we are seeing almost unprecedented gap between feed wheat and feed barley prices – currently almost £50/T. Farmers with sufficient storage and cash flow are hoping that the gap narrows before they need to sell. .

Oilseed Rape and Others

United Oilseeds are estimating the national crop area in 2020 to have been as low as 320,000ha, and with average yields ranging from 2.6 – 3.0t/ha. This would give a crop of under 1m tonnes – less than half that of two years ago.

With the usual cocktail of pests and weather hampering the potential of the OSR crop, there appears to be a trend of farmers moving away from their old three crop rotations to give oilseed rape as long a break as possible. Other crops are finding their way back into the rotation such as linseed and beans. Meanwhile some farmers are looking towards the Countryside Stewardship options such as the “Two Year Legume Fallow (AB15)” which can provide a respectable and much more reliable source of income in place of a traditional break crop.

UK 2021 CROP DRILLING CONSIDERATIONS

As mentioned above there is expected to be a larger than average winter wheat area drilled this autumn.

Farmers are advised not to over-compensate for last year’s poor wheat establishment, as putting a high area into winter cereals this autumn reduces the potential area for further cereals next autumn. Furthermore, the harvest year of 2022 is going to have the added financial burden of BPS payments being cut for the second year in a row, it would be unwise to add insult to injury by forcing the winter crop areas down that year. That said, it is a difficult balance as growers will be seeking to plug gaps in their profit & loss account by reverting to their most reliable performers (which in most cases will be winter wheat). In all cases it will be important to properly address any damage to soils caused last year, in order to maximise chances to harvest a high yielding crop next year.

There will be great temptation this autumn to get the winter crops drilled early, as many farmers will have decided that the risk of black grass and BYDV are problems which can be managed as required and may be less serious than the risk of a second year of low winter wheat areas However, it can be dangerous to “farm for last year”. There are clear benefits to delaying drilling of winter wheat such as the savings in herbicides and fungicides of about £30/ha (FWi).

In terms of oilseed rape, in the south it has so far appeared to be a ‘low pressure’ flea beetle year. Early sown crops (1st week in August) seem to have got away well, without too much flea beetle damage. Perhaps helped by the two week wet spell later that month. Late August and early September sown crops are now just about getting away and although still vulnerable, a reasonable proportion is expected to survive.

LIVESTOCK

Beef and cattle

When the UK went into lockdown the inevitable closing of pubs and restaurants lead to a drop in demand for beef products, and only when the market responded to a heightened demand for beef mince (for home cooking) did the lockdown shock begin to subside.

The beef price had been recovering from very low prices in 2019 and at the beginning of 2020 the outlook was fairly positive, the lockdown initially put that into reverse, but the bounce back pushed prices up above the 5 – year average. This uptick was supported by the easing of lockdown measures that allowed people to enjoy the excellent Barbeque weather.

Since the height of summer, when the ‘eat-out-to-help-out’ scheme was in force, and peak BBQ season was in flow, beef prices have fallen. While deadweight beef prices have fallen beneath those of this time last year they are still about 14p above the 5-year average for late September.

In the longer term however there is no certainty about when the food service industry will be operating at capacity again. With a potential second lockdown (albeit less severe than the first), and with indications that the Irish beef industry is picking up pace there is not much reason to be optimistic about the beef price going into the autumn.

Lambs and sheep

Being seen as a luxury by most households, lamb prices initially suffered from the lockdown, partly due to the food service industry’s pause and slow recovery, but also due to the perception of being a less versatile meat, and where beef mince has won out lamb mince hasn’t fared so well. Added to that one of the mainstays of the lamb annual price cycle are the Islamic feasts which have been subdued affairs this year due to social distancing rules.

Since lockdown eased back in the spring the barbeque effect and eat-out-to-help-out helped prices somewhat. Through the summer however the AHDB have observed roasting joints of lamb become more popular in UK households and the volume of lamb per buyer has increased by 5% on last year – this is great news for lamb producers and marketers who have been trying, for a long time, to reverse the trend of declining supermarket sales.

The longer term outlook for Lamb is a mixed picture, the uncertainty of the Covid-19 situation and Brexit provide little to build a future price consensus on, but both a slowdown in imports from New Zealand and a slowdown in UK production may help support the price somewhat.

Dairy

The struggles of the dairy sector were well reported during the spring, and we all heard the tales of milk being tipped straight out of the parlour into the drain. The government put in place the Dairy Hardship Fund which partly addressed the issue of very poor milk prices from some processors. The differences between the milk processing companies were laid bare as the destination of their milk (supermarket vs. hospitality sector) was the difference between healthy milk prices or a total collapse in demand. Some of this disparity will have been addressed by the re-opening of cafes, restaurants and the eat-out-to-help-out scheme.

The AHDB predicts milk production to pick up this autumn as the autumn calving herds boost numbers back up to normal (many spring calving cows will have been dried off early this year for a combination of factors) feed prices and silage quality fears have been allayed by a good August for grass growth and massive national production of feed barley to provide relatively cheap rations.

The UK average milk price for August 2020 was up to approx. 28ppl (DEFRA).

As with all UK produced commodities Covid-19 has not replaced Brexit as the source of uncertainty it has simply been placed on-top of the stack of destabilising market factors. The future of the dairy market depends on milk processors diversifying their product range and their global export reach.

Dairy Contracts Reform Negotiations

The consultation phase of the Dairy Contracts Reform has now closed. Proposals put forward include an option to introduce fairer pricing mechanisms for dairy farmers ensuring the price paid for milk produced by the farmer is formally agreed in a clear and transparent way.

FERTILISER & FUEL

UK ammonium nitrate is currently priced at around £207/T, and urea is approx. £244/T Guide values for phosphate and potash are: Muriate of Potash (MOP) £248/T, Diammonium Phosphate (DAP) £307/T and Triple Super Phosphate (TSP) £251/T. (all Farmers weekly prices last updated in July 2020).

AHDB data reports red diesel priced at an average of 51.52ppl for August 2020, while diesel at the pump was at 118ppl. This remains significantly below this time last year, due to the coronavirus induced drop in global demand.

POLICY AND REGULATION NEWS

Basic Payment Scheme

The “greening” rules have been removed from the BPS requirements from 2021 onwards. DEFRA and the RPA have made the decision to do away with what was considered an unnecessary over complication of the BPS system. The Ecological Focus Areas (EFA) have been thought to bring very little ecological benefit, and the three crop rule has unfairly penalised farms with smaller arable crop areas.

Greening amendment form: Countryside Stewardship

Farmers can make changes to their Countryside Stewardship Mid Tier or Higher Tier agreements that are due to start on 1st January 2021 due to the scrapping of greening requirements. They can add more land parcels to agreements, increase the amount of land under different options and change the location of the options. Please contact Seb Murray if you would like to discuss Countryside Stewardship or another grant.

“Stepping Stone” Subsidy Scheme

DEFRA minister George Eustice announced in late September that his department are looking into an “Interim Support Scheme” which are will be elements of the ELMS (Environmental Land Management Scheme) released earlier than the original release date of 2024. From 2022 DEFRA will make available a “Sustainable Farming Incentive (SFI)” as a bridge from expiring BPS payments and the new ELMS payments. Read our blog to find out more

DEFRA has set itself a deadline of the end of October for the publication of a document with details of this government plan.

FARM BUSINESS NEWS

NFU calls for Trade Bill to give parliament the ability to ratify or veto new trade deals

The NFU has also called for the House of Lords to adopt an amendment to the Agriculture Bill that would require the recently formed Trade and Agriculture Commission to provide advice to parliament on the impacts of trade deals on UK farming. So far, the government has opposed the vast majority of amendments to the Agriculture Bill and is expected to continue to do so in order to pass the Bill this autumn. The Trade and Agriculture Commission appears almost entirely powerless – it has an advisory role and was only established for six months, which the NFU has come close to admitting when Minette Batters said that if the latest moves were rejected it would be ‘game over’.

Second woodland carbon auction awards contracts to 27 bidders offering 1,517 hectares of new woodlands

The successful bidders will be offered the option to sell the carbon stored by their woodlands to the government over 35 years at a guaranteed price protected against inflation; they do not have to sell their credits to the government, but now have a guaranteed minimum price. The average size of woodland funded in the second auction was 56 hectares, so much bigger than the first auction, and the average price was £19.71 per tonne of CO2e, so lower than the previous average of £24/t. The third auction will take place from 26 October to 1 November and up to 75% of the budget will be ring-fenced for ‘predominantly native woodland’ projects.

Green Homes Grant Scheme funds £2 of every £3 spent on energy efficiency works up to £5,000

The aim of this English scheme is to enable homeowners and landlords to upgrade their homes and properties with energy-saving features, such as insulation or double glazing, in order to reduce energy usage and improve the energy efficiency of a property. Works can include wall and loft insulation, draught proofing and double glazing. These are all works that should improve the Energy Performance Rating (EPC) of a property. A voucher for 100% of the cost up to £10,000 is available for people on low incomes. Other schemes are available in in Scotland, Wales and Northern Ireland. Please contact Jess Waddington, Laura Gibson-Green or your local building surveying team for advice on the grant and, most importantly, to ensure that any measures you are considering are appropriate and effective for your property.

Notice periods of Assured Shorthold Tenancies temporarily increased to six months due to COVID

Notice periods have been extended to six months (until at least 31st March 2021) apart from in certain circumstances: if a tenant has over six months’ rent arrears (now four weeks’ notice period); antisocial behaviour (now same notice period as usual, so two months for an AST). Notices served before the 29th August which gave three months’ notice will remain valid. We will provide a briefing note for landlords and tenants when we have more detail. In Scotland, the ban on evictions is likely to be extended to March 2021. According to research by the National Residential Landlords Association, 87% of tenants have continued to pay full rent since the start of the pandemic.

Review of Countryside Stewardship Facilitation Fund shows it has a range of positive benefits

The review, carried out by FERA for Defra, found that facilitated groups had:

- Improved environmental outcomes through better alignment of option uptake, land manager capability and improved wider environmental management.

- Option richness and diversity were significantly greater in facilitated agreements compared with other AES agreements in the area.

- A positive impact on connectivity of habitats, leading to more resilient landscapes.

- There were also indications that group membership was encouraging uptake of more challenging options

- A wide range of social capital benefits including improved trust, collaboration, communication and relationships.

There is a two page summary of the review that is well worth reading. It feels like facilitated groups, working over landscape or catchment scale, is a good model for the future Environmental Land Management system.

‘Greening’ measures scrapped from 2021 onwards

This means that farmers will not need to comply with the ‘three crop rule’ from next year, nor to allocate land to Ecological Focus Areas. Support payments will not be reduced as the 30% of Basic Payments that was for ‘greening’ will be added to the main payment. This is a welcome simplification in terms of farm management and also as there was little evidence that the measures produced significant environmental benefits.

Contract Farming Agreement survey published for harvest 2019

Total income to the farmer averaged £392/ha and income to the contractor was £395/ha – both above the five-year average. The survey is based on the results of 76 agreements covering more than 20,000 hectares. Our publication also includes our thoughts on how this contract farming agreements will have to become more flexible in response to changes in government support and the introduction of more environmental measures into most arable rotations.

COVID-19 UPDATE

It is clear that Covid-19 will be here for some time to come, at least until a vaccination is developed, and it continues to impose a heavy impact on society and the economy. As alluded to above, the reduction in hospitality events and outlets has greatly reduced demand for milk and meat in particular, but the brewing and malting sectors have also been hit. Rapid changes in the rules regarding social gatherings (and therefore food and drink consumption) make it virtually impossible to plan ahead, and the likelihood is that cases will increase through the winter months.

In most situations the restrictions on work are less severe than on social meetings, but it is important for employers to keep up to date with regulations and guidelines, and to communicate with staff regarding any health issues.

The Chancellor, Richi Sunak, has announced measures to provide further financial support for businesses including the self-employed, and VAT reductions for the hospitality and tourism sectors, which may benefit farm diversification enterprises. The package includes a Job Support Scheme and longer repayment terms for Bounce-Back loans. For further details follow the link: https://www.gov.uk/government/news/chancellor-outlines-winter-economy-plan

Updates on the general rules can be found on the relevant government websites:

ENGLAND: https://www.gov.uk/coronavirus

SCOTLAND: https://www.gov.scot/publications/coronavirus-covid-19-what-you-can-and-cannot-do/pages/overview/